Economic Environment and Advertising Market

Economic Development

According to the International Monetary Fund (IMF), real economic growth in 2014 was at the previous year’s level at 3.3 %. After a good start, the tempo of expansion slowed in the middle of the year due to the restrained economic development in the euro zone and Japan. However, the global economy was supported by resilient growth rates in the USA and Great Britain. Emerging countries likewise continued to grow — although not all with the momentum of previous years. In the fourth quarter of 2014, new impetus was also provided by plummeting oil prices.

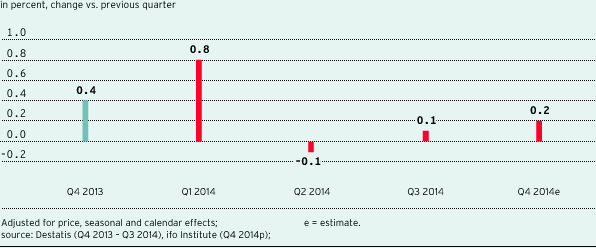

Economic momentum in the euro zone also developed more mutedly than originally expected: After a plus of 0.3 % in the first quarter of 2014 compared to the previous quarter, the growth was a little lower in the next two quarters at 0.1 % and 0.2 %. Although the companies still benefited from more favorable financing conditions, the companies’ propensity to invest was rather slight, because at the same time geopolitical tensions and conservative export forecasts determined the climate. Public and private consumption, on the other hand, generated growth impulses. The ifo Institute expects real quarter-on-quarter growth of 0.2 % in the fourth quarter of 2014 and a growth rate of 0.8 % for 2014 as a whole.

The moderate rate of expansion of the global economy as well as the low momentum in the euro zone also influenced the German economy. After a strong — albeit exaggerated by the construction industry — first quarter of 2014 (+0.8 % as against the previous quarter), the economy stabilized over the rest of the year (Q2: -0.1 % quarter-on-quarter, Q3: +0.1 % quarter-on-quarter). For the fourth quarter the ifo Institute assumes a growth of 0.2 % in comparison to the previous quarter in 2013. Overall, compared to 2013, gross domestic product grew in real terms by 1.5 %. Domestic private consumption in Germany also grew significantly by 1.1 % and essentially strengthened the economy.

Development of gross domestic product in Germany

Development of the TV and Online Advertising Market1

In light of the sound economic development in Germany, the TV advertising market also grew. According to Nielsen Media Research, gross advertising investment in the year as a whole increased by 8.0 % to EUR 13.068 billion (previous year: EUR 12.104 billion). The majority of this occurred in the fourth quarter, in which the most market volume usually accrues.

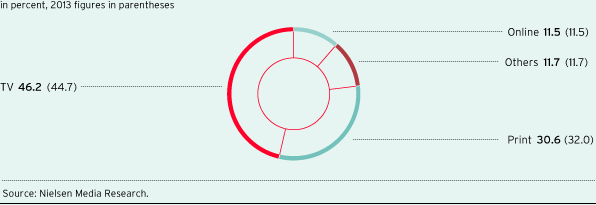

The gross market growth was primarily due to higher TV ad spendings of the Trade (+30.3 %) and Business Services (+25.8 %) industries. At the same time, the German TV advertising market benefited from the high relevance of television as an advertising medium: On a gross basis, the weighting of television in the media mix grew by 1.5 percentage points to 46.2 %. Online media remained constant at 11.5 % (previous year: 11.5 %). The advertising share of print media fell by 1.4 percentage points to 30.6 %.

Media mix German gross advertising market

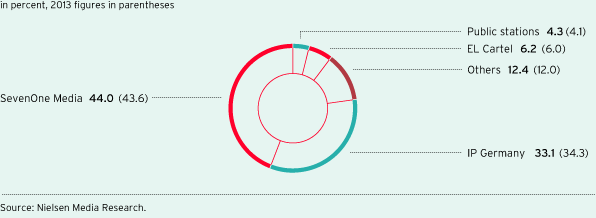

In this positive industry environment, the ProSiebenSat.1 Group significantly increased its TV advertising revenues while extending its market lead over its direct competitors: In 2014 as a whole, SevenOne Media generated gross revenues of EUR 5.754 billion (previous year: EUR 5.281 billion). This is a growth of 8.9 %. At the same time, the market share climbed 0.4 percentage points to 44.0 %. Main competitor IP Deutschland registered a minus of 1.2 percentage points with a market share of 33.1 % (previous year: 34,3 %).

Shares German gross TV advertising market

The gross advertising market of in-stream video ads, which is particularly important for ProSiebenSat.1, continued to grow in 2014. The market grew by 20.1 % to a volume of EUR 375.2 million (previous year: EUR 312.4 million). Thereby the market includes all video advertising shown before, during, or after a video stream. By selling in-stream video ads, SevenOne Media generated gross revenues of EUR 182.4 million after EUR 148.5 million in the previous year. With a market share of 48.6 % (IP Deutschland 32.5 %), SevenOne Media asserted its market leadership. In 2014, gross revenues of EUR 3.249 billion were generated in the German advertising market, which includes besides video advertising further display ads like traditional banners and buttons. This is an increase of 4.0 %.

Advertising spending also developed positively in Austria: Gross television advertising expenditure grew by 10.7 %, compared to the previous year, resulting in EUR 945.2 million. In 2014 as a whole, ProSiebenSat.1 PULS 4 benefited from this positive environment and increased its gross revenues: The marketer reached a gross advertising market share of 35.4 % (previous year: 34.5 %), establishing itself as Austria’s largest TV marketer in gross terms for the second consecutive year.

In Switzerland, gross television advertising expenditure slightly increased in 2014, to CHF 1.188 billion (previous year: CHF 1.174 billion). In this context, ProSiebenSat.1 Schweiz also increased its television advertising revenues; the market share of ProSiebenSat.1 Schweiz reached 25.7 % (previous year: 26.9%).

|

Development of the relevant TV advertising markets for the ProSiebenSat.1 Group |

||||||||

|

|

|

|||||||

|

|

Change against previous year |

|||||||

|

in percent |

2014 |

|||||||

|

||||||||

|

Germany |

8.0 |

|||||||

|

Austria |

10.7 |

|||||||

|

Switzerland |

1.2 |

|||||||

1 Gross advertising expenditure allows only limited conclusions to be drawn about actual advertising revenues as it does not take into account discounts, self-promotion or agency commission. In addition, the gross figures from Nielsen Media Research also include TV spots from media-for-revenue share and media-for-equity deals, which ProSiebenSat.1 does not assign to the Broadcasting German-speaking segment but rather to the Digital & Adjacent segment.